Table of Contents

Spreads versus naked positions

Most professional options traders prefer initiating a spread strategy versus taking on naked option positions. There is no doubt that spreads tend to shrink the overall profitability (max profits), but at the same time spreads give you a greater visibility on risk (max loss).

Always remember “Professional traders value ‘risk visibility’ more than the profits.”

It’s a much better deal to take on smaller profits as long as you know what would be your maximum loss under worst case scenarios.

Another interesting aspect of spreads is that invariably there is some sort of financing involved, wherein the purchase of an option is funded by the sale of another option. In fact, financing is one of the key aspects that differentiate a spread versus a normal naked directional position.

Options Strategies – Bull Call Spread

The Bull Call Spread is quite easy to implement just like Bull Call Spread. A Bull Call spread is implemented when the market outlook is moderately Bullish

Here whole point is that you have probability that its ‘moderately Bullish’, a 4-5% correction would be possible and by invoking a Bull Call spread one would make a modest gain if the markets correct (go down) as expected but on the other hand if the markets were to go up, the trader will end up with a limited loss.

A conservative trader (risk averse trader) would implement Bull Call Spread strategy by simultaneously

- Buying an In the money Call option

- Selling an Out of the Money Call option

There is no compulsion that the Bull Call Spread has to be created with an ITM and OTM option. The Bull Call spread can be created employing any two Call options. The choice of strike depends on the aggressiveness of the trade. However do note that both the options should belong to the same expiry and same underlying. To understand the implementation better, let’s take up an example and see how the strategy behaves under different scenarios.

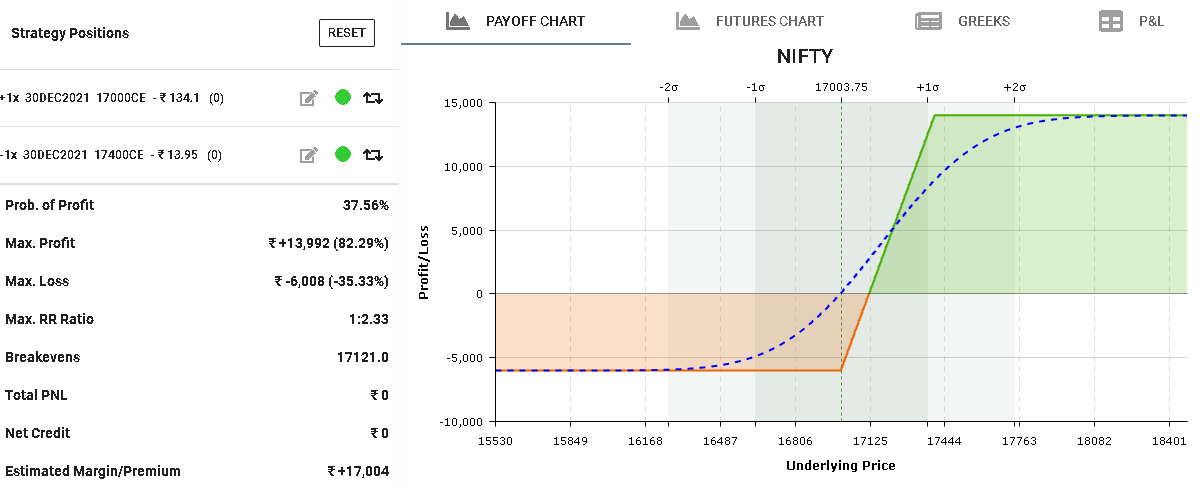

Now say Nifty is at 17000, this would make 17000 CE At the money and 17400 CE Out of the money. The ‘Bull Call Spread’ would require one to sell 17400 CE, the premium received from the sale would partially finance the purchase of the 17000 CE which we buy.

The premium paid (PP) for the 17400 CE is Rs.134.1, and the premium received (PR) for the 17600 CE is Rs.13.95/-. The net debit for this transaction would be 134.1 – 13.95 = -120 around

Scenario’s of trading:

From Opstra Strategy builder here

Overall expectation from the strategy is that the trader gets to make a modest profit when the market goes up while at the same time the losses are capped in case the market goes down.

The losses are capped to 6008 (when markets go down) and the profits are capped to 13,992 (when markets go up)

Strategy makes a loss if the spot moves above the breakeven point, and makes a profit below the breakeven point that is 17121

Both the profits and loss are capped

Spread is difference between the two strike prices.

In this example spread would be 17000 – 17400 = 400

Net Debit = Premium Paid – Premium Received

134.1 – 13.95 = 120 around

Breakeven = Higher strike – Net Debit

17400 – 120 = 17280

Max profit = Spread – Net Debit

400 – 120 = 280

Max Loss = Net Debit

Note: Delta is our freind. Whenever we implement an options strategy always add up the deltas. The delta of 17600 PE is -0.618. The delta of 17400 PE is – 0.342

The negative sign indicates that the Call option premium will go down if the markets go up, and premium gains value if the markets go down. But do note, we have written the 7400 PE, hence the Delta would be0.3420

Deltas are additive in nature we can add up the deltas to give the combined delta of the position. In this case it would be 0.276 adding to – 0.276 = 0

Summary

- Spread offers visibility on risk but at the same time shrinks the reward

- When you create a spread, the proceeds from the sale of an option offsets the purchase of an option

- Bull Call spread is best invoked when you are moderately Bullish on the markets

- Both the profits and losses are capped

- Classic Bull Call spread involves simultaneously purchasing ATM,ITM Call options and selling OTM Call options

- Bull Call spread usually results in a net debit

- Net Debit = Premium Paid – Premium Received

- Breakeven = Higher strike – Net Debit

- Max profit = Spread – Net Debit

- Max Loss = Net Debit

- Select strikes based on the time to expiry

- Implement the strategy only when you expect the volatility to increase