Table of Contents

Option Strategies- what is Iron Condor Strategy

These are captivating times we are living in, especially if you are an alternatives trader in India

Starting 1st June 2020, NSE’s new margin framework is live, which essentially brings down the margin requirement for the hedged position.

What is a hedged position?

Like riding a bike without carrying a helmet. The risk of market-moving against your position, causing capital erosion is high. However, if you hedge your position, then the danger of losing capital reduces drastically. Now, think about this – if your capital loss is minimal, then it implies that the risk for your broking is also minimum right? Now, if the risk for the broking reduces, it also means the risk for the alternate reduces.

So what does this mean to us as a trader?

Remember, the critical margin dynamics – the lesser the risk you carry, the decrease the margin requirement. Higher the risk, higher the margin requirement. Therefore, this means whenever you provoke a hedged strategy, the margins blocked by your broker is less in contrast to the margin required for a naked position.

New margin requirements

Portfolio 1 – Margins have extended for naked unhedged positions to 18.5% from the current 16.7%.

Portfolio 2 – 70% discount in margins for market-neutral positions

Portfolio 3 – 80% reduction in margins for spread positions

What does this imply to you as an options trader? Well, some of the useful strategies, which looked wonderful on paper but were prohibitive to implement due to immoderate margin requirement, now look enticing.

Iron Condor – The iron condor is a four-legged option setup. The iron condor is an improvisation over the short strangle.

Say Nifty is at 9972 , and I’m trying to set up a short strangle by shorting OTM calls and places –

9800 Put at 165.25

10100 Call at 145.25

Since both the options are written/sold, I get to collect a whole premium of 164.25+145.25 = 309.5.

For those of you not acquainted with the strangles, The pay off for this strangle set up is as follows –

As long as Nifty stays within a range, which most often it does. Besides, this is additionally a great way to trade volatility. Whenever you think the volatility has shot up (usually it does round big market events) and therefore the option premiums, then you’d prefer to be an options seller and pocket the high premiums. Short strangles is best for such trades.

In a short strangle, since you sell/write options, it results in a net premium credit. In this case, you get a premium of Rs.23,288/-.

The only difficulty with short strangles is the exposed ends. The strategy bleeds if the underlying asset strikes in either direction. For example, this particular short strangle has a vary of safety between 9490 and 10411. I agree this is a wide enough range, however markets have taught that it can make crazy moves within a quick period. Most recent being the COVID-19 crash in early 2020 followed by rapid recovery from the lows. If you are caught with such a rapid market move, the potential loss can be giant and can wipe your account clean. Now, because the possible loss is unlimited, this means the hazard to you and the broker is quite high.

You can improvise on the brief strangle and set up an iron condor, which in my opinion is a far better strategy. An iron condor improvises a short strangle by using plugging in the open ends. Think of an iron condor in 3 parts –

Part 1 – Set up a short strangle by using selling a slightly OTM Call and Put option

Part 2 – Buy a in addition OTM Call to protect the short call in opposition to a massive market rally

Part 3 – Buy a further OTM Put to defend the short Put against a massive market decline

This makes an iron condor a four-leg alternative strategy. Let us see how this looks –

Part 1 – Sell 9800 PE at 165.25 and sell a 10100CE at 145.25, collect a top rate of 310.5 or Rs.23,288/-.

Part 2 – Buy 10300 CE at 77 to protect the brief 10100 CE

Part 3 – Buy 9600 PE at 105.05 to protect the short 9800 PE

The short choice premium collected finances the lengthy option positions.

Since you buy two options to defend against two short options, the profit plausible reduces to a certain extent –As you can see, the max profit is now Rs.9,634/-, but the decreased profit comes with reduced stress

The max loss is no longer unlimited however restricted to Rs.5,366, which in my opinion is awesome because I now have visibility on danger and it is not open-ended.

The profit is restricted, as long as Nifty stays inside a range, in this case between 9672 and 10228. Notice, the range has shrunk compared to the brief strangle.

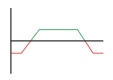

The payoff of an iron condor looks like this –

An iron condor requires you to pay an upfront margin of solely Rs.44,303/-, contrast this with the short strangle’s margin requirement of Rs.1.45,000/-.

Besides, before the new margin framework, executing an iron condor was once not very viable for a retail trader. For these strikes and premiums, the margin requirement for an Iron Condor was roughly in the vary of 2 to 2.2L.

Important things you want to remember while executing an iron condor

The PE and CE that you buy have to have even strike distribution from the sold strike.

For example, here we have sold 9800 PE and 10,100 CE. We have covered the sold strikes by going long on 9600 PE and 10,300 CE. The distinction between 9800 PE and 9600 PE is 200 and 10,100 CE and 10,300 CE is 200. The spread should be even. I cannot defend 9800 PE by buying 9700 PE (difference of 100) and then protect 10,100 CE with 10,300 CE (difference of 200).

The Max loss happens when the market moves either above long CE i.e. 10,300 CE or strikes below long PE i.e. 9,600PE

Spread = 200 i.e. the difference between the bought strike and its protective strike.

Max Profit = Net premium received. In this case, it is 128.45 (9634/75)

Max loss = Spread – Net premium received. In this case, it is 200 – 128.45 = 71.54.

Iron condor trade sequence

- Buy the far OTM call option

- Sell the OTM Call option

- Buy the a long way OTM PUT

- Sell the OTM PUT option

The point here is that you need to have a long position first before initiating the short position. Why? Because long option position is a margin guzzler, so when you have a long position, the device knows the risk is contained and hence will ask you for lesser margins for the Short position.

Summary:

- While the short strangle is an top notch strategy, it has open ends with potentially unlimited losses

- The iron condor is an improvisation over the short strangle

- In an iron condor, the long OTM calls and puts protect the open ends of the short strangle

- Margin required for an iron condor is a long way lesser compared to a short strangle