Table of Contents

Option Strategies – How to do “The Long & Short Strangle” ?

Option Strategies – How to do “The Long & Short Strangle” ?

If you have understood the straddle, then grasp the ‘Strangle’ is quite straightforward. For all practical purposes, the thought method behind the straddle and strangle is quite similar. Strangle is an improvisation over the straddle, mainly to minimize the cost of implementation.

Setup

Nifty is trading at 15921, which would make 15900 the ATM strike. If you have been to set up the long straddle here, you would be required to buy the 15900 CE and 15900 PE.

The premiums for both these alternatives are 66 and 57 respectively.

Net cash outlay = 66 + 57 = 123

Upper breakeven = 15921+123 = 16044

Lower breakeven = 15921 – 123 = 15798

Therefore to set up a straddle, you spend 123 and the breakeven on either side is 2.07% away. As you recognize the straddle is delta neutral, meaning the strategy is insulated to the directional movement of the market. The thought here is that you know that the market will move to a massive extent, but the direction is unknown.

Lower breakeven = 15921 – 123 = 15798

Now from your research you recognize that the market will move (direction unknown) hence you have set up the straddle. However the straddle requires you to make an upfront payment of 123.

Strangle Strategy

The strangle is an improvisation over the straddle. The improvisation on the whole helps in terms of reduction of the strategy cost, then again as a tradeoff the points required to breakeven increases. In a straddle you are required to buy call and put picks of the ATM strike. However the strangle requires you to buy OTM call and put options.

Remember when compared to the ATM strike, the OTM will usually trade cheap, therefore this implies setting up a strangle is less expensive than setting up a straddle. Let’s take an example to explain this higher –Nifty is trading at 17921, to set up a strangle we need to buy OTM Call and Put options.

Note – each the options should belong to the same expiry and equal underlying.

Keep a ratio same, it can be 1:1 ratio meaning 1 lot of call, 1 lot of put option. Or it can be 5:5, which means buy 5 lots of call and 5 a lot of put option.

Going back to the example, considering Nifty is at 17921, we want to buy OTM Call and Put options. I’d prefer to buy strikes which are 200 pts either way (note, there is no particular reason for selecting strikes 200 points away).

So this would mean I would buy 16800 Put choice and 17200 Call option. These options are trading at 28 and 32 respectively.

The combined top class paid to execute the ‘strangle’ is 60.

Let’s figure out how the strategies behave under a number of scenarios.

Scenario’s

1 – Market expires at 17500 (much below the PE strike)At 17500, the premium paid for the call alternative i.e. 32 will go worthless. However the put option will have an intrinsic value of 200 points. The premium paid for the Put alternative is 28, hence the total profit from the put choice will be 200 – 28 = +172

We can further deduct for the premium paid for call alternative i.e. 32 from the profits of Put option and arrive at the overall profitability i.e. 172 – 32 = +140

2 – Market expires at 17640 (lower breakeven)At 17640, the 16800 put option will have an intrinsic value of 60. The put option’s intrinsic value offsets the blended premium paid towards both the name and put option i.e. 32+28 = 60. Hence at 17640, the strangle neither makes money nor losses money.

3 – Market expires at 16800 (at PE strike)At 16800, each the call and put options would expire worthless, hence we would lose the complete premium paid i.e. 32 + 28 = 60. Do note, this also happens to be the most loss the strategy would suffer.

4 – Market expires at 17000, 17200 (ATM and CE strike respectively)Both the options expire nugatory at 17000 and 17200. Hence we would lose the entire premium paid i.e. 60.

5 – Market expires at 17260 (upper breakeven)At 17260, the 17200 Call option has an intrinsic fee of 60, the gains in the call option would offset the loss incurred towards the premium paid towards the call and put options.

6 – Market expires at 17400 (much greater than the CE strike)Clearly at 17400, the 17200 call option would have an intrinsic value of 200 points; consequently the option would make 200 points. After adjusting for the combined premium paid of 60 points, we would be left with one hundred forty points profit. Notice the symmetry of payoff above the upper and below the decrease breakeven points.

Analysis

We can generalize a few things about the ‘Strangle’ –The maximum loss is restricted to the Net premiums paid

The loss would be maximum between the two strike prices

Upper Breakeven point = CE strike + net premium paid

Lower Breakeven point = PE strike – net premium paid

Profit potentially is unlimited, So as long as the market moves irrespective of the direction

Delta and Vega – Both straddles and strangles are similar strategies, therefore the Greeks have a comparable effect on strangle and straddles. Since we are dealing with OTM options (remember we chose strikes that are equidistant from ATM), the delta of each CE and PE would be around 0.3, or lesser.

We could add the deltas of each choice and get a sense of how the overall position deltas behave.

16800 PE Delta @ – 0.3

17200 CE Delta @ + 0.3

Combined delta would be -0.3 + 0.3 = 0 * Simplified for ease of understanding

The combined delta indicates that the approach is directional neutral. The volatility has similar effect on both straddles and strangles.

How the volatility impacts the strangles.

To summarize the impact of Greeks on strangles –

- “The volatility should be relatively low at the time of strategy execution”

- The volatility need to increase during the holding duration of the strategy to be more profitable

- The market should make a large move – the route of the move does not matter

- The expected massive move is time bound, should happen rapidly – well within the expiry

Long strangle is to be setup around main events, and the outcome of these events have to be drastically specific from the general market expectation

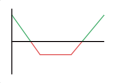

Short Strangle

The execution of a short strangle is the specific opposite of the long strangle. One needs to sell OTM Call and Put options which are equidistant from the ATM strike. In fact you would short the ‘strangle’ for the specific opposite reasons as to why you go long strangle.

Price Outlook – Neutral

Volatility Outlook – Falling

Profit – Limited

Risk – Unlimited

For same strike prices above (the one used in long strangle example) for the short strangle example. Instead of buying these options, you would sell these OTM options to set up a short strangle.

Here is the payoff table of the brief strangle –

the strategy results in a loss as and when the market moves in any unique direction. However the strategy remains profitable between the decrease and upper breakeven points.

Upper breakeven point is at 17260

Lower breakeven point is at 7640

Max earnings is net premium received, which is 60 points

Identify shares which are in a trading range, typically stocks in a buying and selling range form double/triple tops and bottom. Setup the ‘strangle’ by writing strikes which are backyard the upper and lower range. When you write strangles in this backdrop make sure you watch intently for breakouts or breakdowns.

The profits are restricted to the extent of the internet premium received

The profits are maximum as long as the stock stays within the two strike prices

The losses are potentially unlimited

The breakeven factor calculation is the same as the breakeven points of a long strangle, which we have mentioned earlier.

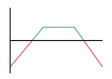

Long Strangle

In this Strategy Long Strangle we buy an out-of-the-money call and an out-of-the-money put option. The call option’s strike price is higher than the underlying asset’s current market price, while the put has a strike price that is lower than the asset’s market price.

Price outlook – Volatile

Volatility – Rising

Profit: Unlimited

Risk: Limited

Few main points

- The strangle is an improvisation over the straddle, the improvisation helps in the strategy cost reduction

- Strangles are delta neutral and is insulated towards any directional risk

- To set up a long strangle one needs to buy OTM Call and Put option

- The most loss in a long strangle is restricted to the extent of the premium received

- The income potential is virtually unlimited in the lengthy strangle

- The short strangle is the exact opposite of the lengthy strangle. You are required to sell the OTM call and put option in a quick strangle

- The Greeks have the same effect on strangles and straddles